Project Management Software for South African Organizations in 2026: A Complete Guide to POPIA Compliance, Deployment Models, and 7 Industry Use Cases

South African organizations spent ZAR 4.2 billion on project management and collaboration software in 2025 according to BMI Research’s enterprise software study, with 41% of organizations larger than 250 employees reassessing their deployment model in response to POPIA enforcement, rand depreciation, and Stage 4-6 load shedding. The Information Regulator‘s 2025 annual report recorded 312 POPIA enforcement notices and ZAR 12 million in administrative fines across the financial, healthcare, public sector, and NGO categories, with 78% of cases citing third-party software platforms as the failure point. Chief Information Officers, IT directors, procurement managers, Information Officers, and operations leaders selecting project management software in 2026 navigate four overlapping pressures simultaneously: POPIA compliance under 8 conditions for lawful processing, deployment model choice between self-hosted and cloud, sector-specific regulatory requirements from 7 industries, and the South African procurement reality spanning 12 to 50 weeks from needs identification to live deployment. This guide covers the South African market landscape, 3 compliance regimes that apply concurrently, 3 deployment models compared, 7 industry use cases with specific requirements, the full procurement journey from week 1 to go-live, 5-year total cost of ownership analysis, and a decision framework directing readers to dedicated guides for deeper analysis.

What is the South African project management software market in 2026?

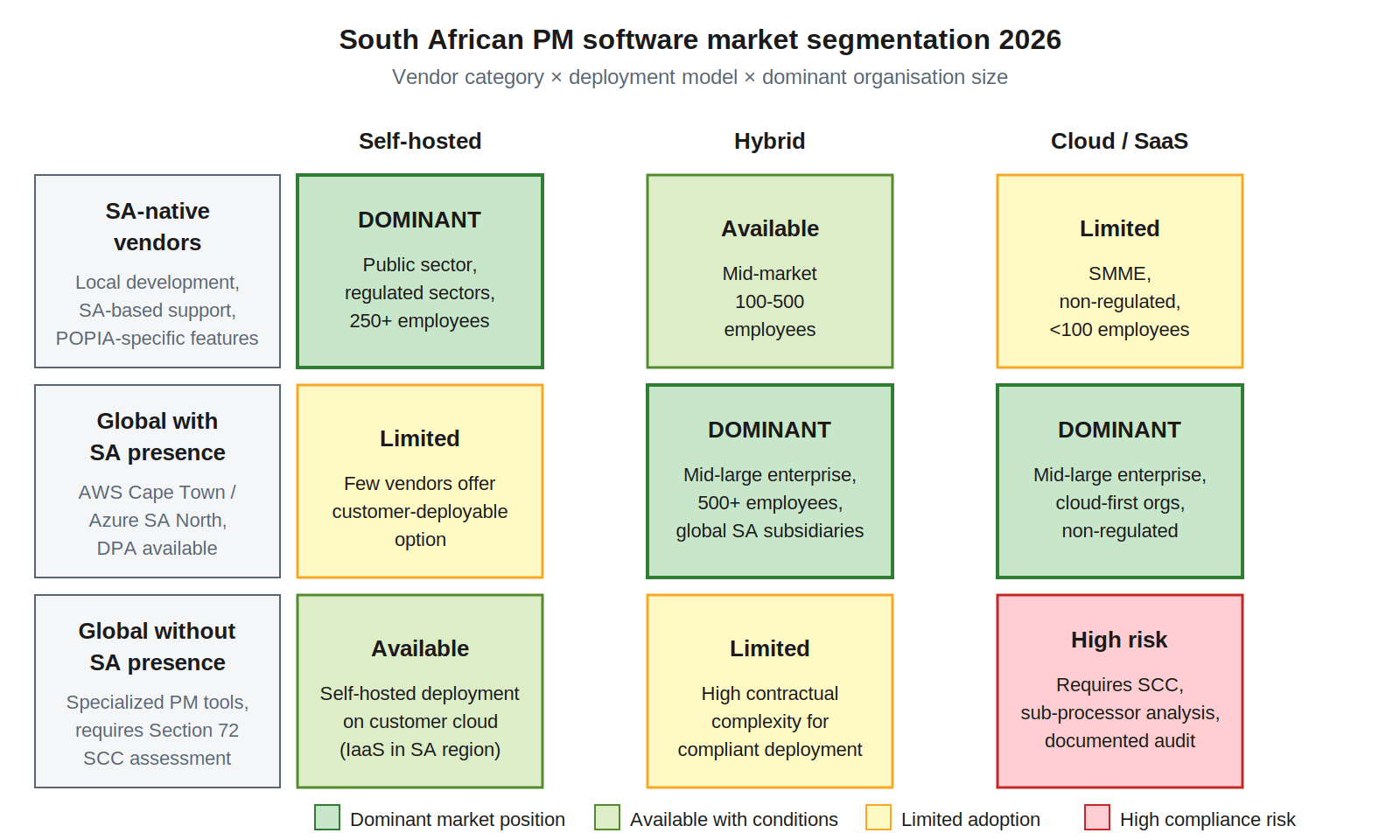

The South African project management software market in 2026 reached ZAR 4.2 billion in annual spending, distributed across three vendor categories — South African native vendors, global vendors with local South African presence, and global vendors without local presence — each holding dominant positions in different deployment models and organization size segments. The 2020-2026 trend shows a structural shift from cloud-only adoption toward self-hosted and hybrid deployment among larger and regulated organizations, while small and non-regulated organizations continue to favour cloud SaaS for operational simplicity.

Three vendor categories shape buyer choice in different ways. South African native vendors — local development teams, South African data centres, and POPIA-specific feature development — hold the dominant position in self-hosted deployment for the public sector and regulated industries. These vendors compete on regulatory fit and local support, accepting smaller global footprint as the trade-off. Global vendors with South African presence — typically operating through AWS Cape Town or Azure South Africa North — dominate hybrid and cloud deployment for mid-large enterprise where global feature parity matters more than POPIA-native design. Global vendors without local presence dominate specialized niches where the product feature set has no local equivalent, requiring self-hosted deployment on customer-controlled cloud infrastructure or substantial contractual engineering for compliant cloud deployment.

Three structural forces drove the shift toward self-hosted and hybrid deployment between 2020 and 2026:

- POPIA enforcement maturation — initial advisory engagement during 2021-2023 transitioned to active enforcement from 2024, with administrative fines becoming the primary tool. Organizations holding sensitive data became materially more cautious about foreign cloud deployment.

- Rand depreciation against vendor billing currencies — averaged 6.4% per year between 2020 and 2025 according to South African Reserve Bank data, compounding USD-billed SaaS costs by approximately 36% over five years and reshaping TCO calculations away from cloud subscriptions.

- Load shedding intensification — Stage 4-6 events became routine across 2024-2026, with rural and non-metro grids experiencing daily extended outages that fundamentally disadvantage cloud-only architectures.

Organization size correlates strongly with deployment preference. Organizations below 100 employees overwhelmingly choose cloud SaaS for operational simplicity, even where POPIA exposure exists. Mid-market organizations (100-500 employees) split across deployment models depending on sector and data sensitivity. Large enterprises (500+ employees) increasingly choose hybrid or self-hosted, with POPIA documentation burden, internal IT capacity, and procurement preference for capital expenditure all favouring this direction.

Which compliance regimes apply to project management software in South Africa?

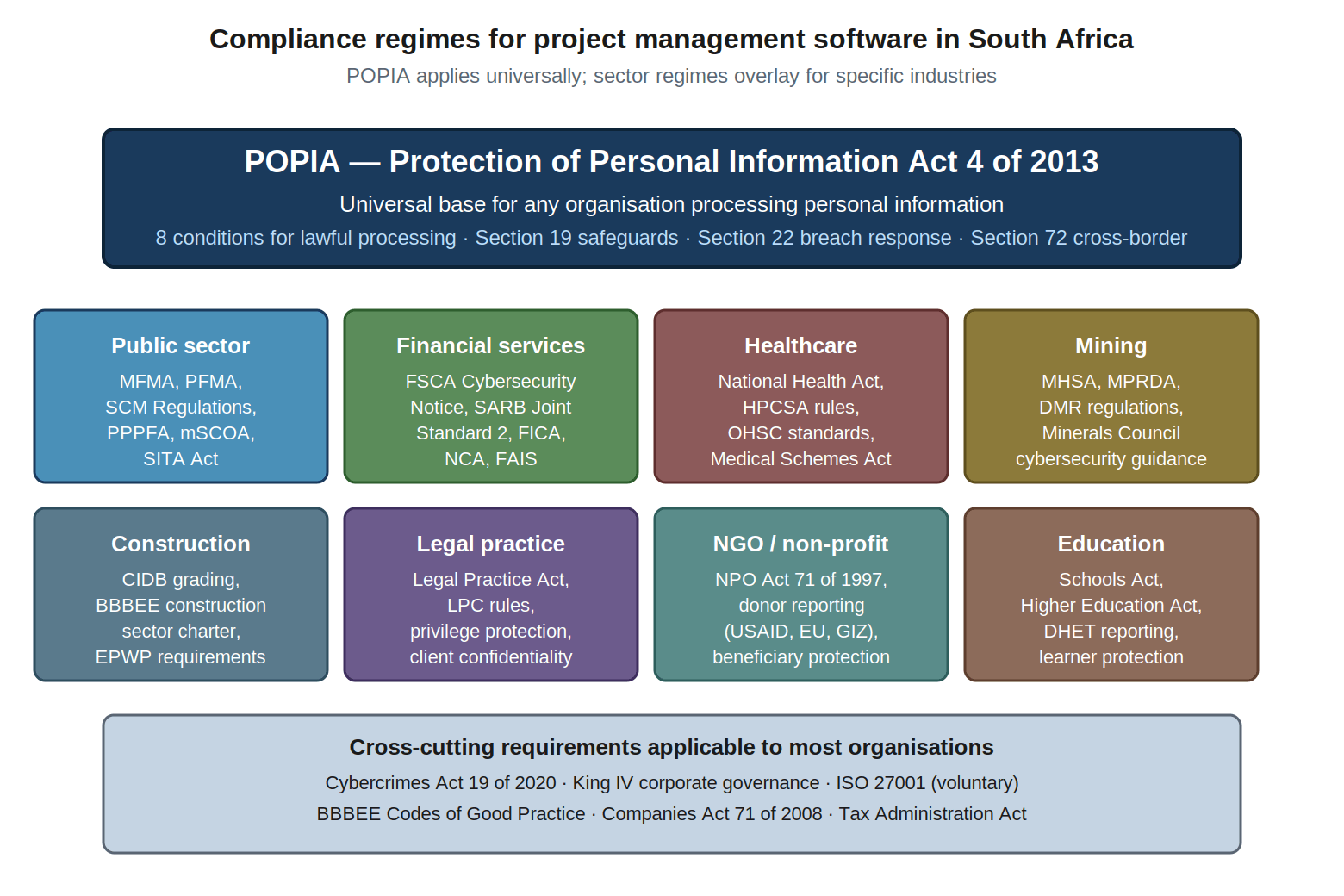

Three concurrent compliance regimes apply to project management software in South Africa: POPIA as the universal base for any organization processing personal information, sector-specific regulations that overlay on POPIA for regulated industries, and cross-cutting requirements affecting most organizations regardless of sector. Each layer adds documentation and control requirements that compound during procurement and ongoing operation.

Figure 2: Compliance regime architecture for project management software. POPIA applies universally; sector regimes overlay for specific industries.

Figure 2: Compliance regime architecture for project management software. POPIA applies universally; sector regimes overlay for specific industries.POPIA is the foundation layer applying to any organization processing personal information, which includes essentially all project management software use cases because the software processes employee, contractor, beneficiary, or client data. The 8 conditions for lawful processing — accountability, processing limitation, purpose specification, further processing limitation, information quality, openness, security safeguards, and data subject participation — must be satisfied regardless of sector. Section 19 establishes 12 specific technical and organisational safeguards expected of compliant systems. Section 22 requires breach notification within 72 hours of detection. Section 72 restricts cross-border transfer to jurisdictions with substantially similar protection or under documented contractual safeguards. The full compliance picture for project management software is covered in our dedicated guide on POPIA-compliant project management software, Section 19 safeguards, and Information Officer duties.

Sector-specific regimes overlay on POPIA for organizations in regulated industries:

- Public sector operates under the Municipal Finance Management Act 56 of 2003, the Public Finance Management Act 1 of 1999, Supply Chain Management Regulations, the Preferential Procurement Policy Framework Act, the Municipal Standard Chart of Accounts (mSCOA), and the State Information Technology Agency Act 88 of 1998. Project management software in public sector context must produce statutory reports, integrate with financial systems, and follow government procurement rules. See the dedicated guide on Project Management Software for South African Municipalities in 2026: LED Tracking, IDP Alignment, and MFMA Reporting Requirements.

- Financial services sit under the Financial Sector Conduct Authority Cybersecurity Notice 2024, the South African Reserve Bank Joint Standard 2 on IT governance effective from June 2024, FICA, the National Credit Act, and FAIS. The combined effect requires documented data residency, sub-processor chain control, breach response capability, and audit-ready records — typically achievable only through self-hosted or carefully-engineered hybrid deployment.

- Healthcare falls under the National Health Act 61 of 2003, the Health Professions Council of South Africa rules of professional conduct, the Office of Health Standards Compliance norms, and the Medical Schemes Act 131 of 1998. Patient information requires documented control over access and storage location, with HPCSA Booklet 12 specifying retention and security expectations.

- Mining operates under the Mine Health and Safety Act 29 of 1996, the Mineral and Petroleum Resources Development Act 28 of 2002, Department of Mineral Resources regulations, and Minerals Council South Africa cybersecurity guidance issued in 2025. The combination addresses worker biometric data, contractor management, and operational security in conflict-sensitive jurisdictions.

- Construction works within the Construction Industry Development Board grading framework, the BBBEE construction sector charter, and Expanded Public Works Programme reporting requirements. Project management software for construction must support CIDB record-keeping, BBBEE compliance evidence, and EPWP worker tracking.

- Legal practice operates under the Legal Practice Act 28 of 2014 and Legal Practice Council Rules. Client confidentiality and privilege protection place practical pressure toward self-hosted deployment for matter management systems, particularly for litigation involving foreign parties.

- NGO and non-profit organizations work under the Nonprofit Organisations Act 71 of 1997, donor-specific reporting requirements (USAID, European Union, GIZ, Global Fund), and beneficiary protection obligations under POPIA Section 26 special personal information rules.

- Education at primary, secondary, and tertiary levels works under the Schools Act 84 of 1996, the Higher Education Act 101 of 1997, Department of Higher Education and Training reporting requirements, and learner protection obligations for under-18 data subjects.

Cross-cutting requirements affect most organizations regardless of sector. The Cybercrimes Act 19 of 2020 criminalises unauthorised access to data and computer systems, creating a parallel criminal track to POPIA’s administrative penalties. King IV corporate governance applies to listed companies and increasingly to large unlisted entities, embedding IT governance expectations in board-level accountability. ISO 27001 certification, while voluntary, provides procurement-defensible evidence of systematic information security management. BBBEE Codes of Good Practice apply to procurement decisions involving most public sector buyers and increasingly to private sector buyers contracting with government. The Companies Act 71 of 2008 and Tax Administration Act 28 of 2011 establish records retention obligations that interact with POPIA’s Section 14 retention principles.

How do deployment models differ in the South African context?

Deployment models — self-hosted, hybrid, and cloud SaaS — differ in the South African context primarily through their relationship to POPIA cross-border transfer rules, the impact of load shedding on continuity, the rand depreciation effect on 5-year total cost of ownership, and the alignment with public sector procurement preferences for capital expenditure over recurring service contracts. The choice is not universal — different deployment models suit different organizational contexts.

Self-hosted deployment places the customer in control of every layer of the technology stack: infrastructure, operating system, application, identity, and data. This removes cross-border transfer analysis entirely because data remains within South African borders and under South African legal authority. Operational continuity through load shedding is materially better because the system runs on UPS-backed local infrastructure independent of internet connectivity. The trade-off is the requirement for internal IT capacity to operate the system, year 1 capital expenditure for infrastructure, and slower elastic scaling than cloud.

Cloud SaaS delegates infrastructure through application to the vendor, leaving the customer responsible only for data, identity, and partial application configuration. This minimises internal IT requirements and provides elastic scaling, at the cost of cross-border transfer documentation burden when the vendor hosts outside South Africa, dependence on internet connectivity for operation, and recurring subscription fees that escalate with rand depreciation against vendor billing currencies. SaaS suits organizations with limited IT capacity, distributed teams without central infrastructure, and lower POPIA exposure from minimal sensitive data holdings.

Hybrid deployment combines elements of both, typically with sensitive data and core application on customer infrastructure and selected functions delegated to vendor infrastructure. Hybrid suits organizations with cloud-friendly subsystems alongside sensitive core operations — regulated financial institutions using cloud collaboration with self-hosted core systems, or NGOs with sensitive beneficiary data but cloud-based external partner portals. The detailed comparison across 8 dimensions including TCO, data sovereignty, security responsibility, and sectoral requirements appears in Self-Hosted vs Cloud Project Management Software in 2026: Data Sovereignty, Total Cost of Ownership, and POPIA Implications for South African Organizations.

What infrastructure realities affect project management software choice?

Four infrastructure realities specific to South Africa affect project management software choice beyond what global vendor evaluation frameworks typically consider: Stage 4-6 load shedding patterns, ISP and fibre availability outside metropolitan areas, the South African data centre landscape, and currency exposure under rand depreciation. Each shapes the practical operating environment in ways that look minor on procurement spreadsheets but materially affect 5-year operational reality.

Load shedding produced 6-10 hours of daily power interruption across most municipalities in 2026, with cellular base stations, fibre exchanges, and remote office connectivity failing concurrently during outages. NERSA’s 2025 annual performance report recorded an average national load shedding intensity of Stage 3.2 across the year, with rural municipalities in Eastern Cape, KwaZulu-Natal, and Limpopo experiencing extended Stage 5-6 windows during winter demand peaks. Cloud-based project management software depends on continuous internet connectivity to vendor infrastructure; self-hosted software on UPS-backed local servers operates independently of external network availability.

ISP and fibre availability vary substantially outside metropolitan areas. Gauteng, Western Cape, and KwaZulu-Natal metro zones generally provide reliable fibre with adequate failover. Non-metro grids in Eastern Cape, Limpopo, Mpumalanga, and Northern Cape often rely on cellular connectivity or single-provider fibre, creating concurrent failure modes during load shedding. Organizations operating across multiple sites face significantly different connectivity profiles per location, which favours deployment models that tolerate intermittent connectivity rather than requiring continuous uptime.

The South African data centre landscape is sufficient for compliant cloud deployment when properly configured. Major facilities include Teraco’s flagship data centres in Johannesburg, Cape Town, and Durban; Vantage Data Centers’ Johannesburg campus operational since 2022; and Africa Data Centres’ multiple South African facilities. Both AWS Cape Town (af-south-1, operational since 2020) and Azure South Africa North (Johannesburg, operational since 2019) provide South African data residency at the infrastructure layer. However, application-layer vendors operating “from South Africa” may store data at any of these facilities or, despite local presence at the application layer, retain underlying data infrastructure in Frankfurt, Dublin, or Northern Virginia.

Currency exposure compounds over 5-year contracts. SaaS subscriptions billed in US dollars typically escalate 8-12% annually under contract terms, with rand depreciation adding 6-7% additional cost pressure based on 2020-2025 currency trajectory. A USD 50,000 annual contract signed in 2021 at approximately ZAR 740,000 would translate to over ZAR 1,100,000 by 2026 even at unchanged USD pricing, before accounting for vendor price increases. South African native vendors and global vendors offering rand-denominated contracts insulate the customer from this exposure entirely.

Which industries have specific project management software requirements?

Seven industries in South Africa apply specific project management software requirements beyond the universal POPIA baseline: municipalities, financial services, healthcare, construction, mining, NGOs, and education. Each industry combines POPIA with sector-specific regulations, operational realities, and stakeholder expectations that shape software selection differently.

| Industry | Primary regulators | Deployment preference | Key software requirements |

|---|---|---|---|

| Municipalities | CoGTA, AGSA, National Treasury | Self-hosted dominant | MFMA s71 reporting, mSCOA integration, IDP/SDBIP alignment, LED tracking, POPIA |

| Financial services | FSCA, SARB Prudential Authority | Self-hosted or hybrid | SARB Joint Standard 2, FSCA Cybersecurity Notice, FICA records, audit trail, ISO 27001 |

| Healthcare | HPCSA, OHSC, Department of Health | Self-hosted or SA-resident cloud | Patient confidentiality, NHA compliance, HPCSA records retention, POPIA s 26 special PI |

| Construction | CIDB, DPWI, sector charter council | Flexible, site-aware | CIDB record-keeping, BBBEE evidence, EPWP tracking, offline-capable site access |

| Mining | DMR, Minerals Council, DMRE | Self-hosted dominant | MHSA reporting, worker biometric protection, contractor management, conflict-sensitive ops |

| NGO / non-profit | DSD, donor agencies | Hybrid or self-hosted | NPO Act compliance, donor reporting (USAID, EU, GIZ), beneficiary protection, offline capability |

| Education | DBE, DHET, CHE | Cloud common, sector-dependent | Learner protection (POPIA s 34), curriculum integration, DBE/DHET reporting |

Three industries currently have dedicated guides in this resource cluster, with the remaining four covered at overview level here pending future expansion. Municipalities — the most regulated industry segment with the highest project management software adoption requirement — appears as a dedicated guide focused on LED tracking, IDP alignment, and MFMA reporting. The NGO and non-profit sector appears as a dedicated guide covering NPO Act compliance, donor reporting frameworks (USAID, EU, GIZ, Global Fund), POPIA beneficiary protection, and field operation considerations. Construction is scheduled for a dedicated guide in subsequent publication cycles based on reader engagement data. Financial services, healthcare, mining, and education are covered at overview level in this pillar; dedicated industry guides may follow as the cluster expands. For complete sector deep-dives, see our guides on project management software for South African municipalities and project management software for South African NGOs.

Two cross-industry patterns deserve attention. First, regulated industries with sensitive data — financial, healthcare, mining, legal — consistently choose self-hosted or hybrid deployment over pure cloud SaaS, with the choice driven by documentation burden and audit defensibility rather than by feature requirements. Second, industries with site-based operations — mining, construction, agriculture, certain NGO field work — value offline capability and load-shedding resilience disproportionately, often more than central-office industries.

What is the procurement journey for project management software in South Africa?

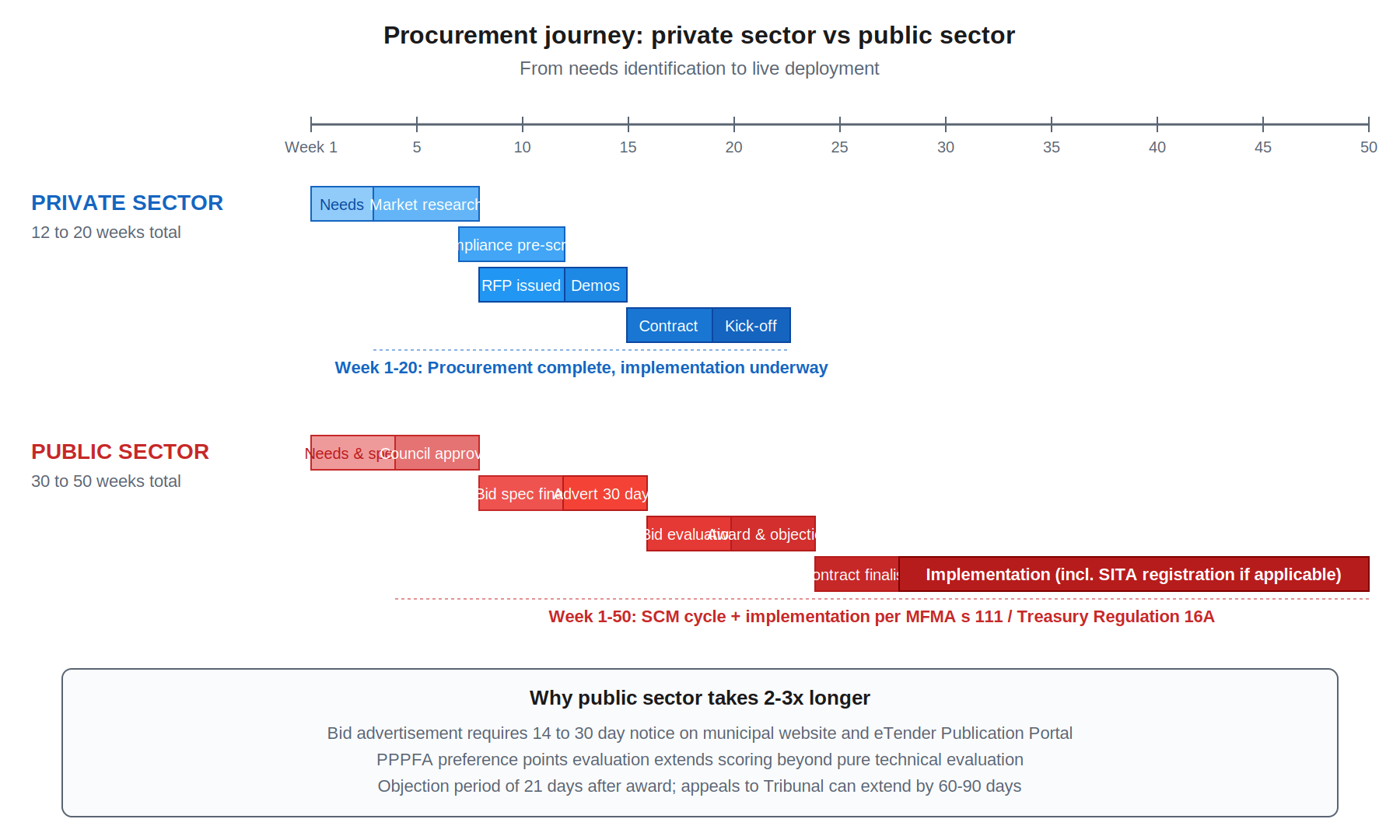

The procurement journey for project management software in South Africa runs 12 to 20 weeks for private sector organizations and 30 to 50 weeks for public sector organizations, with the difference driven primarily by Supply Chain Management Regulations, Preferential Procurement Policy Framework Act preference scoring, and statutory advertisement and objection periods. Understanding the timeline upfront prevents the procurement delays that derail many enterprise software initiatives.

Private sector procurement breaks into seven phases:

- Weeks 1-3: Needs assessment — stakeholder interviews, functional requirements documentation, current state analysis, business case approval at executive level.

- Weeks 4-6: Market research — vendor longlist of 10-15 candidates, initial vendor briefings, comparison against high-level requirements.

- Weeks 5-7: Compliance pre-screening — POPIA assessment per vendor, sector-specific compliance check, sub-processor disclosure review, contractual safeguard availability.

- Weeks 7-9: RFP issued — formal request to a shortlist of 3-5 vendors with detailed evaluation criteria, response window of 2-3 weeks.

- Weeks 10-12: Vendor demos and technical evaluation — structured demonstrations against scripted scenarios, sandbox access, reference customer interviews.

- Weeks 13-16: Contract negotiation — commercial terms, Data Processing Agreement execution, service level agreement, exit and portability provisions.

- Weeks 17-20: Implementation kickoff — project team mobilisation, data migration planning, integration design, user acceptance testing preparation.

Public sector procurement adds five additional phases driven by regulatory requirements:

- Weeks 1-4: Needs assessment and specification — same as private sector but with formal technical specification document required for the bid file.

- Weeks 5-8: Internal approvals — IT steering committee, council or board approval, budget allocation confirmation, SCM committee briefing.

- Weeks 9-12: Bid specification finalization — preference points framework, evaluation criteria, technical specifications signed off by accounting officer.

- Weeks 13-16: Bid advertisement — 14-day notice for contracts above ZAR 200,000; 30-day notice for contracts above ZAR 1 million, published on the municipal website and National Treasury eTender Publication Portal.

- Weeks 17-20: Bid evaluation — administrative compliance check, technical evaluation, BBBEE verification, preference points calculation under PPPFA Regulations 2022.

- Weeks 21-24: Award and objections — bid adjudication committee recommendation, accounting officer approval, 21-day objection period during which unsuccessful bidders may appeal.

- Weeks 25-28: Contract finalization — formal contract execution, SLA finalization, BBBEE certificate filing, contract register entry.

- Weeks 29-50: Implementation — same scope as private sector but with SITA registration where applicable, additional governance touchpoints, and broader stakeholder coordination across departments.

Three factors stretch public sector timelines beyond the documented minimums. Objection appeals to the Tender Defaulters and Restricted Suppliers Tribunal can extend the award phase by 60-90 days. National Treasury intervention on contracts of strategic significance can trigger additional review. Section 36 deviation paths — used where standard SCM processes are impractical — require explicit justification and post-award reporting to council, AGSA, and Treasury, with risk of subsequent finding of irregular expenditure if not properly documented. For comprehensive public sector procurement deep-dive, future expansion will produce a dedicated guide on government procurement under MFMA, PPPFA, and SITA Act.

What does 5-year total cost of ownership look like in South Africa?

Five-year total cost of ownership for project management software in South Africa breaks across 8 cost categories, with self-hosted deployment typically lower than cloud SaaS at organisation sizes above 100 users due to perpetual licence economics and rand depreciation effects. The break-even point between deployment models occurs between year 2 and year 3 for most mid-large organisations.

The 8 cost categories that comprise comprehensive TCO are software licensing (including support and maintenance fees), server hardware (initial and refresh cycle), backup and continuity infrastructure (UPS, generators, backup storage), implementation and integration services, internal IT operations capacity, training and change management, currency depreciation factor for foreign-billed contracts, and exit costs at contract termination or vendor change. Generic vendor TCO calculators typically include the first three categories and omit the remainder, producing systematic understatement of cloud SaaS costs and overstatement of self-hosted costs.

For a 250-user mid-large enterprise across five years, illustrative TCO figures distribute approximately as follows. Self-hosted deployment runs ZAR 1.5-2.0 million total, weighted toward year 1 capital expenditure with lower years 2-5 ongoing cost. Cloud SaaS runs ZAR 2.5-3.0 million total, distributed evenly across years with escalation. Hybrid sits between at ZAR 2.0-2.5 million. The precise figures vary substantially by vendor, licence model, integration scope, and internal IT cost basis, but the relative ordering between deployment models is consistent across the market. The detailed TCO table with category-by-category breakdown appears in our Self-Hosted vs Cloud Project Management Software in 2026: Data Sovereignty, Total Cost of Ownership, and POPIA Implications for South African Organizations guide.

Three TCO factors are routinely under-modelled in procurement evaluations:

- Rand depreciation compounds over 5-year contracts at approximately 6-7% annually based on 2020-2025 trajectory. A USD 50,000 annual contract increases by approximately 36% in rand terms over 5 years at unchanged USD pricing.

- Exit cost appears late in vendor relationships and can absorb several months of subscription fees through data export charges, format conversion, parallel operation during migration, and historical record retention requirements.

- Internal IT operations capacity for self-hosted deployment can be either absorbed by existing teams or quantified as additional FTE cost. The honest accounting is the latter for procurement comparison purposes.

How should South African organizations build their project management software evaluation framework?

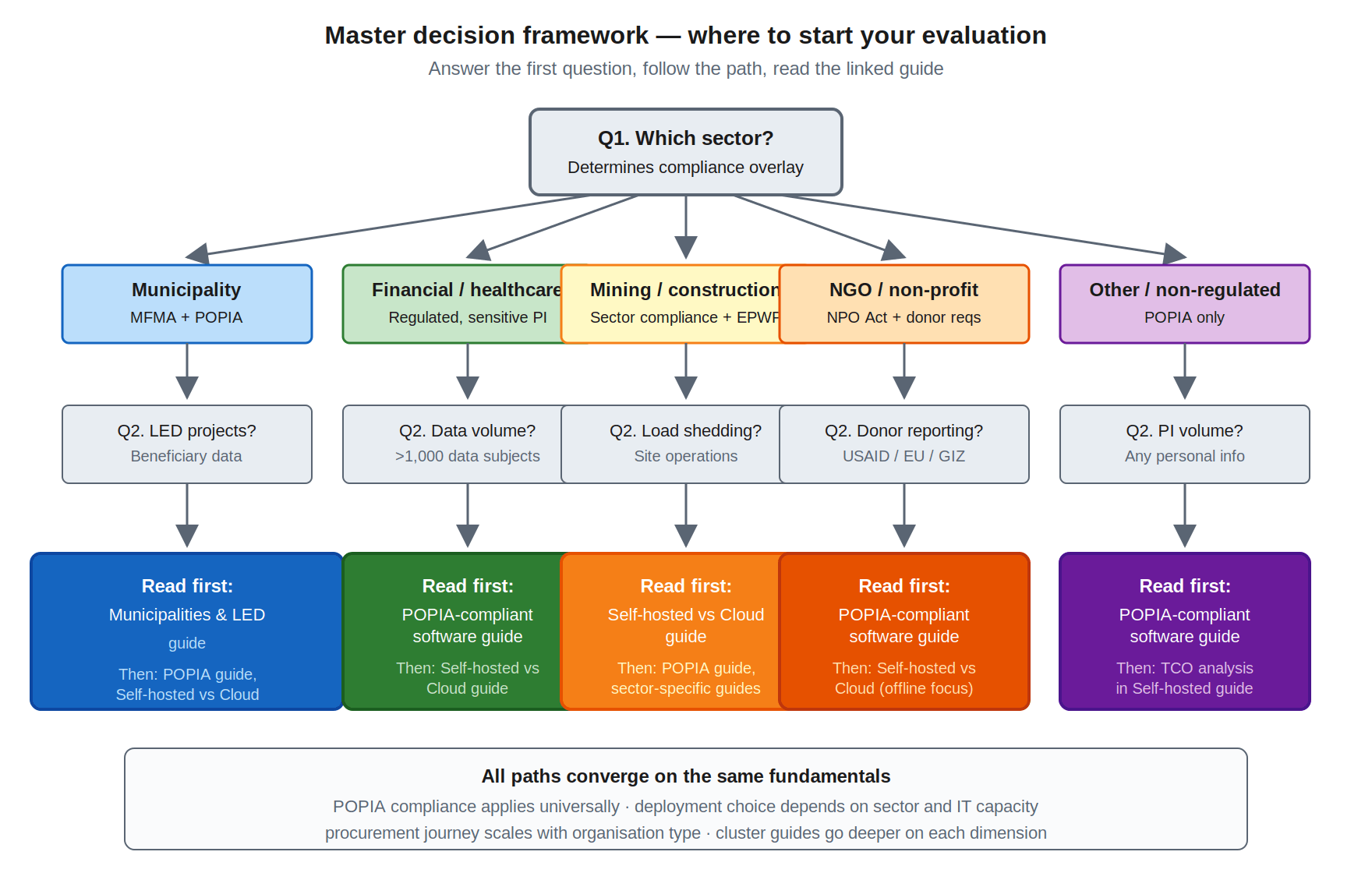

South African organizations should build their project management software evaluation framework around their specific sector, data sensitivity, infrastructure context, and growth horizon, using the master decision flowchart below to identify which dedicated guides apply to their situation. The framework treats POPIA compliance as a universal baseline, deployment choice as a context-dependent decision, and sector-specific requirements as overlays that shape but do not override the fundamental evaluation.

The framework treats sector as the first-level filter because compliance overlay determines the bulk of evaluation criteria. Once the sector is identified, the second-level filter narrows further:

- Municipalities with LED projects involving beneficiary data should start with the municipalities and LED guide, then progress to POPIA-compliant software and self-hosted vs cloud comparison.

- Financial services and healthcare with regulated personal information at scale (>1,000 data subjects) should start with the POPIA-compliant software guide, then read self-hosted vs cloud for deployment evaluation.

- Mining and construction with site operations affected by load shedding should start with self-hosted vs cloud (focusing on offline operation and infrastructure resilience), then read POPIA compliance and sector-specific guidance.

- NGO and non-profit with donor reporting requirements should start with the POPIA-compliant software guide, then read self-hosted vs cloud (focusing on offline capability for field operations).

- Non-regulated organizations with any personal information processing should start with the POPIA-compliant software guide for baseline compliance, then evaluate deployment based on TCO and operational fit.

All paths ultimately converge on the same fundamentals: POPIA compliance applies universally, deployment choice depends on sector and IT capacity, procurement journey scales with organization type, and cluster guides go deeper on each dimension. The framework is iterative — initial procurement based on current circumstances may need revisiting as the organization grows, expands into regulated activities, or experiences changing infrastructure constraints. A 5-year reassessment cycle aligned with typical contract terms ensures the deployment model remains fit for purpose.

Frequently asked questions

What is the most-used project management software in South Africa?

The most-used project management software in South Africa varies by organisation size and sector. Cloud SaaS tools including Microsoft Project, Asana, Monday.com, and ClickUp dominate small and non-regulated mid-market segments. South African self-hosted vendors including Kendo Manager hold dominant position in the public sector and regulated industries. No single platform leads across all segments.

Does South African project management software need to be developed locally?

South African project management software does not need to be developed locally to be POPIA-compliant. POPIA addresses how personal information is processed, not where the software is developed. International software can be POPIA-compliant when properly configured and deployed; locally-developed software is not automatically compliant. Verification of compliance applies to both equally.

How much does project management software cost for a South African organization?

Project management software costs for a South African organisation range from approximately ZAR 200 per user per month for cloud SaaS at small scale to ZAR 80 per user per month equivalent for self-hosted deployment at 250+ user scale over a 5-year contract. Total 5-year TCO for a 250-user organisation typically falls between ZAR 1.5 million and ZAR 3.0 million depending on deployment model and vendor.

Is Asana or Monday compliant with POPIA?

Asana and Monday.com can be configured for POPIA compliance through customer-side controls, Data Processing Agreement execution, and Standard Contractual Clauses for cross-border data transfer. Neither is automatically POPIA-compliant out of the box. The Information Officer assessment, sub-processor analysis, and contractual safeguards documentation remain customer responsibilities regardless of vendor compliance posture.

How long does it take to implement project management software in a South African organization?

Implementation of project management software in a South African organisation typically takes 4-8 weeks for cloud SaaS deployment in a non-regulated organisation, 8-16 weeks for self-hosted deployment with standard integrations, and 16-26 weeks for public sector deployment including SITA registration where applicable. These windows exclude the preceding procurement journey of 12-50 weeks.

What is the difference between SaaS and self-hosted project management software in the South African context?

SaaS project management software is vendor-hosted and vendor-operated, accessed through the browser; the customer controls only data and identity. Self-hosted software runs on customer infrastructure with the customer operating all layers. In the South African context, self-hosted addresses POPIA cross-border transfer eliminating jurisdictional risk, operates through load shedding on UPS-backed servers, and aligns with public sector capital expenditure procurement preferences.

Which industries have the strictest project management software requirements in South Africa?

Financial services and healthcare have the strictest project management software requirements in South Africa due to combined POPIA, sector-specific regulation, and operational risk profiles. Public sector follows closely due to MFMA reporting and AGSA audit exposure. Mining and legal practice apply selective strict requirements driven by data sensitivity rather than blanket regulation. NGO and education vary widely by donor or institutional requirements.

Can a South African organization use international project management software?

A South African organisation can use international project management software provided POPIA Section 72 is satisfied through one of five mechanisms: adequacy of the destination jurisdiction, data subject consent, contract necessity, data subject benefit, or adequate contractual safeguards. The Information Officer must document the assessment, the contract should include POPIA-aligned Standard Contractual Clauses, and verification of actual data centre location is the practical step most often overlooked.

South African organisations selecting project management software in 2026 face a more complex evaluation environment than at any prior point in the local market’s history. POPIA enforcement now produces administrative fines rather than advisory engagement, rand depreciation reshapes 5-year TCO calculations away from cloud subscriptions, Stage 4-6 load shedding fundamentally disadvantages cloud-only architectures in non-metro grids, and sector-specific compliance overlays compound the documentation burden for regulated industries. The four-dimension evaluation framework — POPIA compliance, deployment model, sectoral requirements, and procurement reality — converts software selection from a feature-driven vendor conversation into a structured procurement assessment defensible against AGSA, Information Regulator, and internal governance scrutiny. This pillar guide provides the overview; the dedicated cluster guides referenced throughout provide the depth at each dimension.